TD Bank posted $266-million in after-tax restructuring charges through measures including job cuts and real estate reductions.Fred Lum/the Globe and Mail

Canadian banks are slashing jobs to curb mounting expenses and taking higher loan loss provisions as they grapple with the threat of an economic slowdown.

Some of the country’s largest lenders reported mixed fourth-quarter earnings results, with Royal Bank of CanadaRY-T and Canadian Imperial Bank of CommerceCM-T posting higher profit on Thursday that beat analyst expectations, while Toronto-Dominion Bank reported lower net income that missed estimates.

Each bank outlined plans to restructure their operations – measures that include work-force reductions and trimming their real estate footprints – as they look to rein in rising costs ahead of a potential economic slowdown.

TD TD-T posted $266-million in after-tax restructuring charges through measures including job cuts and real estate reductions. The lender expects to book savings of about $400-million pretax in 2024.

The bank said it will reduce its work force by 3 per cent. In the fourth quarter ended Oct. 31, the bank shed about 0.5 per cent of its employee base, or more than 500 jobs. Chief financial officer Kelvin Tran said the restructuring charges also include plans to accelerate the bank’s transition to new technology platforms and reduce its corporate and branch real estate premises.

“We saw the opportunity to undertake a restructuring program to streamline and deliver efficiencies that enabled us to create capacity to invest for future growth,” Mr. Tran said in an interview.

Also Thursday, CIBC recorded $114-million in severance charges, capping off the fiscal year with a 5-per-cent reduction in full-time staff.

RBC said in its third-quarter results that its total number of employees fell 1 per cent from the previous quarter, and that it expected to further decrease its work force by 1 per cent to 2 per cent in the fourth quarter.

On Thursday, the bank said that it posted a severance charge of $157-million as its work force dropped by 2.5 per cent, trimming 2,355 jobs. RBC expects savings of $235-million starting in the next quarter, and that growth in expenses should drop from double-digit increases to low- to mid-single digits in 2024.

RBC earned $4.1-billion, or $2.90 per share, a 6-per-cent jump from the same period last year as a surge in capital markets earnings and lower taxes offset climbing loan-loss provisions. CIBC booked $1.5-billion, or $1.53 per share, a 25-per-cent increase as provisions for bad loans were lower than analysts anticipated and retail banking profits rebounded.

TD however posted a 57-per-cent drop in profit to $2.9-billion, or $1.49 per share, as higher expenses and acquisition and integration costs from its takeover of New York-based investment bank Cowen Inc. sent capital markets profit plunging.

CIBC’s share price climbed 5.1 per cent and RBC’s stock rose 3.2 per cent, while TD slumped 0.7 per cent on Thursday in Toronto.

On Tuesday, Bank of Nova ScotiaBNS-T posted lower profit that missed analyst expectations. Bank of Montreal BMO-T and National Bank of Canada NA-T will release results on Friday.

As delinquencies recover from their lows in 2021, Canada’s largest lenders are increasing their provisions for credit losses – the funds banks set aside to cover loans that may default. RBC set aside $720-million for potentially sour loans, more than analysts expected. TD and CIBC reserved $878-million and $541-million respectively, less than analysts expected.

“The environment this quarter was more stable,” CIBC chief financial officer Hratch Panossian said in an interview. “Things like forward view of debt-service ratios based on the view of interest rates, which started shifting a bit this quarter. And unemployment continues to be generally fairly strong.”

TD investors are waiting for details on the fines or other penalties stemming from probes by regulators and law-enforcement agencies, including the U.S. Department of Justice, related to its anti-money-laundering practices that derailed its acquisition of Tennessee-based First Horizon Corp.

The lender said Thursday that it does not yet know the outcomes of the inquiries and investigations, but it expects monetary and non-monetary penalties. However, it expects that the actions will not have a material impact on the bank’s financial condition. Analyst estimates on the potential penalty range between US$500-million and $1-billion.

“Notwithstanding the progress we have made in our U.S. business, it was disappointing that some shortcomings in our anti-money-laundering control environment were identified during the year, which we are working hard to address, and I am confident that in time we will,” TD chief executive officer Bharat Masrani said in fourth-quarter filings. He added that while the decision to terminate the deal “was a difficult decision – and one not taken lightly – it was the right one for the bank under the circumstances.”

RBC is still in the midst of acquiring the Canadian subsidiary of Britain-based banking giant HSBC Holdings PLC after the foreign company decided to exit the market. Despite escalating scrutiny from political opposition parties and environmental and other stakeholder groups, RBC said it still expects the deal to close in the first quarter of 2024.

“All parties in the approval process understand the benefits to the country of tax revenue and dividend increases, of investment in Canada and incremental investment in Canada, of the benefits to employees and to clients – everybody understands that,” RBC chief executive officer Dave McKay said during a conference call with analysts. “Everybody understands that HSBC has made a choice to leave, and it would look horrible on Canada if you didn’t allow the free flow of capital.”

Prime Minister Justin Trudeau defended his government's economic performance Thursday by touting investments in housing and dental care when asked about new data that shows the economy actually contracted in the last quarter.

Statistics Canada reported this morning that the Canadian economy shrank at an annualized pace of 1.1 per cent in the third quarter — a performance much worse than what some forecasters expected for the July through September period.

In October, the Bank of Canada forecast that the economy would actually grow by roughly 0.8 per cent in that quarter.

Finance Minister Chrystia Freeland's fall economic statement, tabled last week, cited a September survey of private sector economists projecting the economy would grow at least a little in the third quarter. The weak economic performance could undermine that document's fiscal projections.

The new StatsCan data suggests the economy is underperforming even the relatively pessimistic growth projections from the central bank and others.

The slump was driven in part by reduced exports, including a steep decline in refined petroleum energy products, StatsCan said.

Conservative Leader Pierre Poilievre pounced on the poor data, saying Trudeau has "led the economy into a ditch."

The negative economic growth comes after the Bank of Canada went on an aggressive rate-hiking campaign to drive down red-hot inflation.

WATCH | Trudeau addresses shrinking Canadian economy in 3rd quarter

Trudeau addresses shrinking Canadian economy in 3rd quarter

7 hours ago

Duration 2:16

Featured VideoPrime Minister Justin Trudeau said the government is investing in housing and affordability after Statistics Canada reported the country's GDP shrank 0.3 per cent in the third quarter.

The intended effect of this effort — an economic slowdown to restore price stability — appears to be panning out.

"We know that Canadians are facing challenging times and have for a long stretch now," Trudeau said.

"That's why we've been stepping up with direct supports for Canadians," he said, citing past GST rebates and rental relief for low-income Canadians.

Trudeau said Ottawa would push ahead with a housing accelerator fund, a program that floats money to cities that cut building-related red tape to get more units built.

Prime Minister Justin Trudeau and Deputy Mayor of Ajax Marilyn Crawford arrive for a housing announcement in Ajax, Ont. on Thursday, Nov., 30, 2023. (Christopher Katsarov/Canadian Press)

He said the government would come through with more low-cost loans for homebuilders to get affordable rental homes built to help deal with the country's acute housing crunch.

He also said the federal dental care program for children, and a forthcoming expansion of rhe program for eligible seniors, will save families money when every extra dollar counts.

Trudeau claimed that Ottawa is managing its finances in "a fiscally responsible way" and the federal government could come through with more relief for Canadians if the economy slips into a recession and unemployment rates move higher.

"We have room to respond if there is more to do," Trudeau said.

"We have the lowest deficit in the G7, the best debt-to-GDP ratio in the G7."

He accused Poilievre of planning to quickly eliminate the federal deficit through harmful cuts to public services. "Conservatives propose cuts in services and programs as a way of creating growth, which makes absolutely no sense," Trudeau said.

Poilievre warns of 'stagflation' risk

While Canada's debt servicing costs are lower than those faced by some other countries, Freeland's fall economic statement warns that they are expected to balloon.

With interest rates at a 20-year high, the cost to borrow to carry the federal government's $1.2-trillion debt has spiked from $20.3 billion in 2020-21 to $46.5 billion in this fiscal year.

Poilievre said Canada could be facing "stagflation" — high inflation combined with high unemployment and slack demand for goods and services.

WATCH | Poilievre, Anand spar over new economic numbers

Poilievre, Anand spar over new economic numbers

7 hours ago

Duration 1:27

Featured VideoConservative Leader Pierre Poilievre said the U.S. economy is 'roaring' while Canada's is 'snoring.' Treasury Board President Anita Anand dismissed what she called 'trite rhymes' and touted the Liberals' economic plan.

The inflation rate has levelled off in recent months and the country's unemployment rate is still relatively low at 5.7 per cent.

And while the third quarter GDP figure was a big miss, Statistics Canada did revise up its numbers for the second quarter.

The statisticians at the federal agency now say the economy grew by 1.4 per cent in the April-June period, higher than the figure they previously reported.

But Poilievre said Canada's record just doesn't compare to what's transpired in the U.S.

"Why is it that the American economy is roaring while the prime minister's economy is snoring?" Poilievre said in question period.

Treasury Board President Anita Anand said the International Monetary Fund (IMF) projects that Canada will have the highest economic growth in the G7 next year.

Rachel Bendayan, the parliamentary secretary to the minister of Finance, said the Conservatives are "talking down" the economy while the Liberals are focused on their economic plan, which includes delivering more homes and boosting climate-friendly industries.

Industry Minister Francois-Philippe Champagne also responded to Conservative criticism by touting a recent multi-billion dollar investment by Dow, a U.S. chemical company, in Fort Saskatchewan, Alta.

"There's one number the Conservatives never mentioned. We're third for foreign direct investment," Champagne said. "This is how you lead a country. This is how you lead an economy."

Three of Canada's biggest lenders posted quarterly earnings on Thursday, and as was the case at Scotiabank earlier in the week, they're all putting a lot more money aside to cover loans that might go bad.

Royal Bank, TD Bank and CIBC revealed their financial results to investors before stock markets opened on Thursday, and while all three remain very profitable, they all showed a sharp uptick in the amount of money they're setting aside to cover bad loans, a closely watched banking metric known as provisions for credit losses.

At Royal Bank, Canada's biggest lender set aside $720 million to cover loans that either aren't currently being paid back as planned, or the bank is worried might soon be. That figure is up by 89 per cent from $381 million a year ago.

At TD, the bank set aside $878 million in provisions, an increase of 42 per cent from $617 million this time last year.

At CIBC, the bank set aside $541 million. That's an increase of 24 per cent from last year's level.

Loan loss provisions at the first two were worse than analysts were expecting, but at CIBC they actually came in lower than some forecasts.

WATCH | How a slowdown in the economy will impact your personal finances:

Why slowing inflation and interest rates might not mean more money in your pocket

1 month ago

Duration 3:17

Featured VideoThe Bank of Canada's decision to hold at its current interest rate might mean the worst of the punitive rate hikes might be over. However CBC's Rob Brown explains why it might not mean immediate relief for your wallet.

While the uptick in troubled loans is a concern, the figures are a drop in the bucket when viewed against the backdrop of the overall financial picture at all three lenders

At Royal Bank, the bank posted a quarterly profit of $4.13 billion, up from $3.88 billion a year earlier, and raised its dividend to $1.38 per share — up from $1.35 previously.

At TD, profit fell from $6.67 billion to $2.89 billion but it, too, felt confident enough to increase its payout to shareholders to 1.02 per share, up from 96 cents previously.

CIBC also raised its dividend to 90 cents per share, up from 87, as its profits increased from $1.19 billion to $1.48 billion.

Job cuts

TD did announce, however, that it is taking a $363-million restructuring charge during the quarter, relating to severance and other costs.

The bank said in filings it plans to cut its its current full-time work force by about three per cent. In TD's case, that works out to just over 3,000 people.

In a presentation to investors, CIBC said it has cut as much of five per cent of its full-time employees in its past fiscal year. That's almost 2,400 people.

RBC and Scotia have previously announced similarly sized layoffs.

Dominique Lapointe, director of macro strategy for Manulife, says that Canada's biggest banks are closely tied to the interest rate picture and overall economic environment, and that's playing out in their outlooks right now

"In the next couple of quarters, we think for the sector in general, it's going to be a tougher economic environment," he said in an interview Thursday. "That doesn't mean that this will lead to any sort of massive changes into the employment picture but for sure, some difficulties ahead.

"If and when interest rates start to be lower ... banks will face stronger profits and are going to reduce their provisions for potential losses."

Three of Canada's biggest lenders posted quarterly earnings on Thursday, and as was the case at Scotiabank earlier in the week, they're all putting a lot more money aside to cover loans that might go bad.

Royal Bank, TD Bank and CIBC revealed their financial results to investors before stock markets opened on Thursday, and while all three remain very profitable, they all showed a sharp uptick in the amount of money they're setting aside to cover bad loans, a closely watched banking metric known as provisions for credit losses.

At Royal Bank, Canada's biggest lender set aside $720 million to cover loans that either aren't currently being paid back as planned, or the bank is worried might soon be. That figure is up by 89 per cent from $381 million a year ago.

At TD, the bank set aside $878 million in provisions, an increase of 42 per cent from $617 million this time last year.

At CIBC, the bank set aside $541 million. That's an increase of 24 per cent from last year's level.

Loan loss provisions at the first two were worse than analysts were expecting, but at CIBC they actually came in lower than some forecasts.

While the uptick in troubled loans is a concern, the figures are a drop in the bucket when viewed against the backdrop of the overall financial picture at all three lenders

At Royal Bank, the bank posted a quarterly profit of $4.13 billion, up from $3.88 billion a year earlier, and raised its dividend to $1.38 per share — up from $1.35 previously.

At TD, profit fell from $6.67 billion to $2.89 billion but it, too, felt confident enough to increase its payout to shareholders to 1.02 per share, up from 96 cents previously.

CIBC also raised its dividend to 90 cents per share, up from 87, as its profits increased from $1.19 billion to $1.48 billion.

TD did announce, however, that it is taking a $363-million restructuring charge during the quarter, relating to severance and other costs.

The bank said in filings it plans to cut its its current full-time work force by about three per cent. In TD's case, that works out to about 3,000 people.

RBC and Scotia have previously announced similarly sized layoffs.

The federal Liberals avoided a catastrophe Wednesday when Heritage Minister Pascale St-Onge announced the government had struck a deal with Google for it to pay media outlets for the news content on its platforms.

The Liberals want to frame the deal as a big win — that Ottawa successfully pressured the tech giant to submit to a new law that requires it to financially support journalism in this country to the tune of $100 million a year. They want to be seen as a “pioneer” in this space, a model for other countries to follow.

Ottawa has agreed to set a $100-million yearly cap on payments that Google will be required to make to media companies when the government's controversial online news legislation takes effect at the end of the year.

The announcement Wednesday has the Liberals bending to the tech giant's demands after Google threatened back in February to remove news from its platform.

The Online News Act compels tech giants to enter into compensation agreements with news publishers for content that generates revenue for companies such as Google by appearing on its sites.

Broadcasters and French-language and Indigenous news organizations would join newspapers in being eligible for the deals, with draft regulations suggesting the amount of money would be linked to the number of full-time journalists on staff.

A formula in the government's draft regulations to implement the bill would have seen Google contribute up to $172 million to news organizations. Google balked, saying it was expecting a figure closer to $100 million, based on what it said was a previous estimate from Canadian Heritage officials.

The company appears to have got what it wanted after an extended period of negotiation.

Still, Canadian Heritage Minister Pascale St-Onge called it a "historic development," insisting Wednesday that the agreement was ultimately a win for the government and for the local news publishers it is seeking to support.

"We have found a path forward to answer Google's questions about the process and the act. Google wanted certainty about the amount of compensation it would have to pay to Canadian news outlets," she said on Parliament Hill.

"Canada reserves the right to reopen our regulations if there are better agreements struck elsewhere in the world," she added.

St-Onge also noted that the $100-million figure will be indexed to inflation.

Google's president of global affairs, Kent Walker, thanked the minister for "acknowledging our concerns and deeply engaging in a series of productive meetings about how they might be addressed."

He said in a statement that the "extensive discussions" addressed the company's "core issues" with the bill.

"While we work with the government through the exemption process based on the regulations that will be published shortly, we will continue sending valuable traffic to Canadian publishers," Walker said.

The deal will allow Google to comply with the legislation by paying into a single collective bargaining group that will serve as a media fund.

Meta, on the other hand, complied simply by blocking all news content from Canadian users of its largest platforms, Instagram and Facebook. A statement from the company Wednesday suggested that hardline approach hasn't changed.

"Unlike search engines, we do not proactively pull news from the internet to place in our users’ feeds and we have long been clear that the only way we can reasonably comply with the Online News Act is by ending news availability for people in Canada."

Prime Minister Justin Trudeau said he was satisfied with the agreement with Google and held out hope that Meta would eventually come around.

"Unfortunately, Meta continues to completely abdicate any responsibility towards democratic institutions and even stability," he said, "but we’re going to continue to work positively in those areas."

Last month, News Media Canada — a lobby group for hundreds of Canadian newspapers and magazines — said it agreed with many of the issues Google raised during the back-and-forth over how the bill would be implemented.

The group said there should be a cap on how much the search giant would have to pay under the law.

But Friends, an advocacy group for Canadian broadcasters, said the deal doesn't deliver the kind of support for journalism that it had been hoping to see.

"We will be looking to the regulations to ensure that smaller, independent, and equity-seeking media groups are assured access to funding," executive director Marla Boltman said in a statement.

An official with the Canadian Heritage Department said the final regulations for the law, which are due by mid-December, will also address Google's other concern that the law establishes linking to news sites as the basis for payment.

The official said final regulations will clarify that Google's payment is to help news publishers and broadcasters, and not for news links.

CBC and Radio-Canada will also get a portion of the $100 million, but that will be determined once regulations are finalized.

In addition to its financial contribution, Canadian Heritage said Google will continue to make programs available for Canadian news businesses, such as training, tools and resources for business development and support for non-profit journalism projects.

Google said Wednesday that the deal means there will be immediate changes to existing agreements it has with publishers in Canada under its Google News Showcase agreements, which were part of a $1-billion global investment.

The company said it will review its ongoing investments in Canada when the final regulations are published.

Google wouldn't say how much it is already paying publishers under existing contracts, saying such agreements are confidential commercial arrangements.

Companies that fall under the Online News Act must have total global revenue of $1 billion or more in a calendar year, "operate in a search engine or social-media market distributing and providing access to news content in Canada" and have 20 million or more Canadian average monthly unique visitors or average monthly active users.

For now, Google and Meta are the only companies that meet those criteria.

This report by The Canadian Press was first published Nov. 29, 2023.

Google has agreed to pay Canadian news businesses $100 million a year to comply with the country's Online News Act, despite previously saying it would remove Canadian news links from search rather than make the required payments.

Google and government officials agreed to a deal that lets Google negotiate with a single news collective and reduce its overall financial obligation. Facebook owner Meta is meanwhile holding firm in its opposition to payments.

"Google will contribute $100 million in financial support annually, indexed to inflation, for a wide range of news businesses across the country, including independent news businesses and those from Indigenous and official-language minority communities," Minister of Canadian Heritage Pascale St-Onge said in a statement today.

The $100 million in Canadian currency is worth about $74 million in US currency. Before today's deal, the federal government estimated that Google would have to pay $172 million a year.

"After extensive discussions, the Canadian Government agreed to a number of changes to address our deeply held concerns that C-18 would require payment for links and create uncapped financial liability through an unworkable bargaining process, simply for helping Canadians find relevant and useful information," Google said in a statement provided to Ars.

The C-18 law contains a "duty to bargain" requiring large search engines and social media services to negotiate payments with news businesses or groups of news businesses. In June, six months before the law's implementation, Google said it would not pay the "link tax" and instead would remove links to Canadian news sources from Google Search and Google News for users who access the services in Canada.

Payments based on number of journalists

Today, Google thanked St-Onge "for acknowledging our concerns and deeply engaging in a series of productive meetings about how they might be addressed." The resulting deal provides "a streamlined path to an exemption at a clear commitment threshold," Google said.

"While we work with the government through the exemption process based on the regulations that will be published shortly, we will continue sending valuable traffic to Canadian publishers," Google said.

The Canadian government confirmed that Google will be allowed to negotiate with a single collective, instead of separately with multiple news organizations or groups of news organizations. "Google will have the option to work with a single collective to distribute its contribution to all interested eligible news businesses based on the number of full-time equivalent journalists engaged by those businesses," St-Onge said.

New rules to effect the change will be implemented before the Online News Act is enforced. St-Onge's announcement said the Canadian Heritage agency "will share more details about the final regulations following approval by the Treasury Board of Canada and prior to the Act coming into effect on December 19, 2023."

Google said that "under the revised regulations, there is a path for publishers to continue to receive valuable traffic... which Google can allocate through a deal with a single collective of its choosing. Importantly, this will allow Google to bypass the requirement to settle with publishers directly or individually, and any corresponding mandatory bargaining obligations."

No Canadian news on Facebook

Meta, the other company affected by the Online News Act, "ended its talks with the government last summer and stopped distributing Canadian news on Facebook and Instagram," the CBC noted today.

Meta hasn't changed its stance. "Unlike search engines, we do not proactively pull news from the Internet to place in our users' feeds and we have long been clear that the only way we can reasonably comply with the Online News Act is by ending news availability for people in Canada," Meta told the CBC.

Canadian officials previously estimated that Facebook would have to pay $62 million a year, but the deal with Google suggests that Meta could lower that amount significantly. Meta reportedly hasn't resumed talks with the government.

"This [deal with Google] shows that this legislation works," St-Onge said, according to the CBC. "Now it's on Facebook to explain why they're leaving their platform to disinformation and misinformation instead of sustaining our news system."

Ottawa and Google have reached a deal regarding how much the search giant will pay to Canadian media companies in an apparent settlement of an ongoing dispute over the Online News Act.Photo by Richard Drew/The Associated Press

Article content

Today’s top headlines

Article content

4:55 p.m.

Market close: Bond yields fall on signs Federal Reserve is in ‘sweet spot’

Advertisement 2

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world's leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world's leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Article content

The rally that’s driving global bonds to their best month since 2008 gained further traction, with Treasuries climbing on bets the United States Federal Reserve will start cutting interest rates in the first half of 2024.

Hopes for a Fed pivot intensified after economic data emboldened the so-called Goldilocks scenario. Two-year yields dropped 10 basis points to 4.64 per cent. Fed swaps priced in a quarter-point rate cut by May.

The S&P 500 wavered near “overbought” levels. Nvidia Corp. joined gains in chipmakers, Tesla Inc. whipsawed in the run-up to its Cybertruck event and Microsoft Corp. fell. Oil climbed ahead of a high-stakes OPEC+ meeting.

Gross domestic product rose at the fastest pace in nearly two years, while consumer spending advanced at a less-robust rate. The Fed’s preferred inflation metric — the personal consumption expenditures price index — was revised lower. U.S. economic activity slowed in recent weeks as consumers pulled back on discretionary spending, the Fed said in its “Beige Book.”

Bonds extended their November rally on speculation the Fed is done with its aggressive hiking cycle. A Bloomberg gauge of global sovereign and corporate debt has returned about five per cent this month, heading for its best performance since the depths of the recession in December 2008 — when the Fed cut rates to as low as zero and pledged to boost lending to the financial sector following the collapse of Lehman Brothers Holdings Inc.

Advertisement 3

Article content

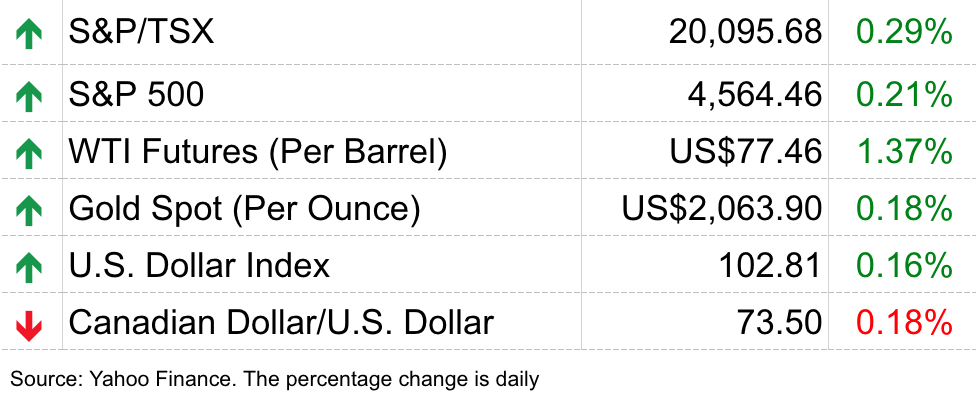

In New York, the Dow Jones industrial average was up 13.44 points at 35,430.42. The S&P 500 index was down 4.31 points at 4,550.58, while the Nasdaq composite was down 23.27 points at 14,258.49.

The S&P/TSX composite index closed up 79.43 points at 20,116.20.

Bloomberg

3:20 p.m.

Labour shortages cost small businesses $38 billion in lost sales in 2022: CFIB

A hiring sign is posted outside a retailer at the Cornwall Centre in Regina.Photo by KAYLE NEIS/Regina Leader-Post files

Small businesses lost more than $38 billion in revenue opportunities last year because of labour shortages, according to estimates from the Canadian Federation of Independent Business.

CFIB economist Laure-Anne Bomal says staffing shortages led to some employers working more hours, reducing their hours of operation and refusing services or contracts.

Bomal says while the number doesn’t indicate the Canadian economy lost billions of dollars, it is still a significant amount of revenue that small businesses could have benefitted from.

The report says small businesses in the construction sector saw the biggest loss in potential business opportunities, estimated to top $9.6 billion last year, followed by the retail sector losing out on an estimated $3.8 billion and social services with a $3.3 billion loss.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don't see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 4

Article content

Regionally, small businesses in Ontario posted the highest potential revenue opportunity losses in 2022, estimated at $16 billion, followed by Quebec and Alberta.

CFIB offered solutions in its report including work-integrated learning in high school for youth, labour mobility of core workers aged 24-64 and tax credits for career extensions among other policy suggestions.

The Canadian Press

1:57 p.m.

Google to pay $100 million a year to Canadian news publishers in deal with Ottawa

Alphabet Inc.’s Google is set to contribute $100 million a year to Canadian news publishers, in a deal that has the Liberal government bending to the tech giant’s demands after it threatened to remove news from its platform.

Canadian Heritage Minister Pascale St-Onge announced today that the federal government has reached a deal with Google that will benefit the news sector.

Ottawa has agreed to set a $100-million yearly cap on payments the company will be required to make to media companies when the Online News Act takes effect at the end of the year.

The law will compel tech giants to enter into agreements with news publishers to pay them for the news content that appears on their sites, if that content contributes to revenues.

Advertisement 5

Article content

The amount announced today is what Google said it expected to pay, and the figure is 41 per cent lower than the amount that would’ve been required under a formula in the government’s draft regulations.

The deal also allows Google to pay into a single collective bargaining group that will serve as a media fund.

The Canadian Press

1:50 p.m.

Bank of Canada survey participants largely oppose creating a digital loonie

Loonies with the effigy of King Charles are struck at an event at the Royal Canadian Mint in Winnipeg.Photo by John Woods/The Canadian Press files

The central bank released its findings today, which show that more than 80 per cent of respondents strongly oppose the Bank of Canada researching and building the capability to issue a digital dollar.

The vast majority of respondents also say they do not trust the Bank of Canada to issue a secure digital currency.

Among the top concerns of respondents was privacy, with the questionnaire revealing low levels of trust in institutions to protect their personal data.

The Bank of Canada notes the findings do not necessarily reflect the views of the overall public because participants self-selected to respond to the questionnaire.

Advertisement 6

Article content

While the public consultations aimed to gauge interest in a digital currency, the central bank says the decision to create a digital dollar is for Parliament to make. Find out more.

The Canadian Press

1 p.m.

Ottawa to select Boeing military plane in sole-source deal, bypassing Bombardier: sources

The federal government is expected to announce that it has selected Boeing Co. to replace the military’s aging patrol planes.Photo by Justin Tang/The Canadian Press files

The federal government is expected to announce as early as Thursday that it has selected Boeing Co. to replace the military’s aging patrol planes in a multibillion-dollar deal, according to three sources familiar with the matter.

The decision to go with a sole-source contract would close the door on Quebec-based business jet maker Bombardier Inc., which has been pushing for an open bid.

The sources, who were not authorized to speak publicly on the matter, say that last week cabinet green-lit the purchase of 16 P-8A Poseidon surveillance aircraft to replace the half-century-old CP-140 Auroras.

They say the Treasury Board held a special meeting last night and approved the contract, which a U.S. agency has listed at $US5.9 billion.

The procurement department has stated that Boeing’s off-the-shelf reconnaissance plane is the only one available that meets Royal Canadian Air Force requirements, particularly around submarine-hunting technology.

Advertisement 7

Article content

Bombardier has argued that its alternative — currently a prototype — would offer a cheaper and more high-tech aircraft that’s made in Canada.

The Canadian Press

12:33 p.m.

Midday markets: Treasury yields slide on Federal Reserve bets as stocks wobble

The rally that’s driving global bonds to their best month since 2008 gained further traction, with Treasuries climbing on bets the United States Federal Reserve will be able to start cutting rates in the first half of 2024.

Hopes for a Fed pivot intensified after economic data emboldened the so-called Goldilocks scenario. Two-year yields dropped seven basis points to 4.67 per cent. Fed swaps priced in a quarter-point rate cut by May.

The S&P 500 wavered after an advance that drove the gauge toward one of its biggest November rallies on record. Megacaps were mixed, with Nvidia Corp. leading gains in chipmakers and Microsoft Corp. sliding. Oil rose ahead of a high-stakes OPEC+ meeting.

Multiple block trades supported a steepening of the U.S. curve, with yields on short-dated Treasuries falling more than those on longer securities. Such trades are set to benefit as the U.S. moves closer to rate cuts.

Advertisement 8

Article content

In New York, the Dow Jones industrial average was up 9.20 points at 35,426.18. The S&P 500 index was up 3.07 points at 4,557.96, while the Nasdaq composite was up 3.97 points at 14,285.73.

In Toronto, The S&P/TSX composite index was up 40.36 points at 20,077.13.

Bloomberg

12:04 p.m.

Alberta oil executives head to COP28 climate summit

A logo of the COP28 is pictured ahead of the United Nations climate summit in Dubai on November 28, 2023.Photo by GIUSEPPE CACACE/AFP via Getty Images

Executives and senior leaders from Canada’s oil and gas sector are heading to Dubai for the upcoming United Nations COP28 climate talks.

The Pathways Alliance consortium of oilsands companies and the Canadian Association of Petroleum Producers are among the groups who will be at the climate summit representing this country’s fossil fuel industry.

The Pathways Alliance says it is going to the summit because it recognizes the oilsands is a significant emitter of greenhouse gases.

The group says it wants to tell the world it is committed to being part of the solution. It says it’s eager to talk about some of its emissions reduction plans, including a proposal to spend $16.5 billion to build a massive carbon capture and storage network in northern Alberta.

Advertisement 9

Article content

Janetta McKenzie of clean energy think-tank the Pembina Institute says there’s a growing recognition by the oil and gas sector that it must do more to combat emissions if it wishes to remain competitive in the future.

But she says observers of COP28 need to be on the lookout for greenwashing, as many oil and gas companies have so far made a lot of climate promises but have yet to invest the tens of billions of dollars it will take to see those promises through.

The Canadian Press

11:42 a.m.

Ottawa reaches deal with Google over controversial Online News Act

The federal Liberal government has reached a deal with Google over the Online News Act, following threats from the digital giant that it would remove news from its search platform in Canada.

A government official confirmed that news to The Canadian Press under condition of anonymity, because they were not authorized to speak publicly about the deal.

CBC News is reporting, citing an unnamed source, that the agreement would see Canadian news continue to be shared on Google’s platforms in return for the company making annual payments to news companies in the range of $100 million.

Advertisement 10

Article content

A formula in the government’s draft regulations for the bill would have seen Google contributing up to $172 million to news organizations — but Google had said it was expecting a figure closer to $100 million based on a previous estimate.

The legislation, which comes into effect at the end of the year, requires tech giants to enter into agreements with news publishers to pay them for news content that appears on their sites, if it helps the tech giants generate money.

Google had warned that it would block news from its search engine in Canada over the legislation, as Meta Platforms Inc. has already done on Instagram and Facebook.

The Canadian Press

11:09 a.m.

AbCellera, company that helped develop COVID-19 treatment, to lay off 10 per cent of workforce

The treatment AbCellera developed, in partnership with U.S. pharmaceutical giant Eli Lilly, is meant for high-risk individuals — such as the elderly — who’ve contracted COVID-19 but don’t yet have severe symptoms.Photo by AbCellera

The Vancouver-based company that helped develop the first antibody therapy treatment for COVID-19 has announced layoffs amounting to 10 per cent of its workforce.

AbCellera Biologics Inc., announced the cuts in a filing to the United States Securities and Exchange Commission.

The filing says the layoffs and reorganization will help it “focus its efforts toward the clinical development of new antibody medicines for patients.”

Advertisement 11

Article content

In May, AbCellera announced a $701-million infrastructure project to boost the overall scope of its Vancouver manufacturing plant.

The company said the plan, backed by more than $375 million in federal and British Columbia funding, also included clinical trials.

AbCellera’s statement to the SEC says it estimates it will incur approximately US$2.5 million in cash expense related to the layoffs but, with more than US$1 billion in available liquidity, it says it has sufficient capital to “execute on its strategy” beyond the next three years.

The Canadian Press

10:21 a.m.

Markets open: Stocks rise as ‘Goldilocks narrative continues’

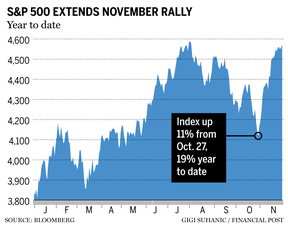

Stocks extended one of their biggest November rallies on record amid bets the Unites States Federal Reserve will pull off a soft landing as the economy remains fairly strong and inflation shows signs of cooling.

All major groups in the S&P 500 advanced, with the gauge approaching 4,600 and heading toward its highest since July.

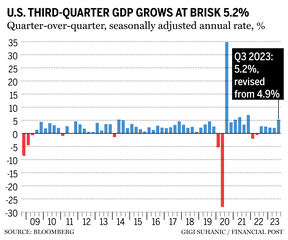

Gross domestic product rose at an upwardly revised 5.2 per cent annualized pace in the third quarter, the fastest in nearly two years. Consumer spending advanced at a less-robust 3.6 per cent rate. The Fed’s preferred inflation metric — the personal consumption expenditures price index — was revised down to a 2.8 per cent annual rate in the third quarter. Excluding food and energy, the gauge was also marked lower to 2.3 per cent.

Advertisement 12

Article content

To John Leiper at Titan Asset Management, the data highlighted the strength of the economy. Meantime, the drop in the core PCE price index will be interpreted by Fed officials as a sign their strategy remains on track and they may well achieve a soft landing scenario. “The Goldilocks narrative continues for now,” he said.

On Wall Street, the S&P 500 was up 0.39 per cent at 4,572.64. The Dow Jones Industrial Average was up 0.06 per cent at 35,435.12 while the Nasdaq composite was up 0.37. per cent at 14,334.60.

In Toronto, the S&P/TSX composite index was up 0.21 per cent at 20,078.35. Read more.

Bloomberg

9 a.m.

U.S. economy grows at fastest rate in two years

Shrugging off higher interest rates, America’s consumers spent enough to help drive the economy to a brisk 5.2 per cent annual pace from July through September, the government reported Wednesday in an upgrade from its previous estimate.

The government had previously estimated that the economy grew at a 4.9 per cent annual rate last quarter.

Wednesday’s second estimate of growth for the July-September quarter confirmed that the economy sharply accelerated from its 2.1 per cent rate from April through June. It showed that the U.S. gross domestic product — the total output of goods and services — grew at its fastest quarterly rate in nearly two years.

Advertisement 13

Article content

The Associated Press

8:10 a.m.

Enbridge to boost dividend

Enbridge Inc says it expects its business to continue to grow next year.Photo by Paul Morden/Postmedia Network

Enbridge Inc. is raising its dividend as it expects its business to continue to grow next year.

The company also reaffirmed its full year guidance for 2023 for earnings before interest, income taxes and depreciation and distributable cash flow.

Enbridge says it will pay a quarterly dividend of 91.5 cents per share, effective with the dividend payable on March 1, 2024, up from 88.75 cents per share.

The increased payment to shareholders will come as the company expects 2024 adjusted EBITDA on its base business to total $16.6 billion to $17.2 billion. Distributable cash flow per share is expected between $5.40 and $5.80.

Enbridge says the ranges for 2024 represents growth of four per cent for its base business EBITDA and three per cent for its distributable cash flow compared with the midpoint of its 2023 guidance.

The guidance does not include the impact of the U.S. gas utility acquisitions announced in September that are expected to close during 2024.

The Canadian Press

7:30 a.m.

OECD warns world headed for deepening slowdown

Advertisement 14

Article content

The world’s advanced economies are heading into a deepening slowdown, the OECD warned today.Photo by Postmedia

The world’s advanced economies are heading into a deepening slowdown as markedly higher interest rates take a hefty toll on activity that could still become more acute, the OECD warned.

Growth is losing momentum in many countries and won’t edge up until 2025, when real incomes recover from the inflation shock and central banks will have begun cutting borrowing costs, the Paris-based organization said.

It forecasts global gross domestic product to expand only 2.7 per cent next year after an already weak 2.9 per cent in 2023. The pace will only pick up to 3 per cent in 2025, according to the assessment.

Moreover, the OECD said the risks to the forecast are tilted downwards amid heightened geopolitical tensions, an uncertain outlook for trade, and the risk that tight monetary policy could hurt firms, consumer spending and employment more than expected.

It expects interest rate cuts in the United States will only begin in the second half of 2024, and not until the spring of 2025 in the euro area. That contrasts starkly with the expectations of markets, which are currently pricing the Federal Reserve and the European Central Bank will ease policy as soon as the first half of next year.

Stocks are rising this morning on expectations that the Federal Reserve is done with policy tightening and may start cutting interest rates next year.

The optimism comes after Fed Governor Christopher Waller suggested the central bank is well positioned to push inflation to a 2 per cent target. Billionaire investor Bill Ackman also said Tuesday he’s betting Fed cuts could come as soon as the first quarter — earlier than market pricing is suggesting.

Oil climbed for a second day as traders awaited a high-stakes OPEC+ meeting on supply. Gold extended gains to its highest level since May, also buoyed by hopes of a Fed policy shift.

Bloomberg

What to watch today

Ottawa will hold a briefing on Canada’s priorities and objectives for the United Nations Climate Change Conference, taking place in Dubai, United Arab Emirates, from Nov. 30 to Dec. 12.

In data out today, the United States gets a reading on gross domestic product and the release of the Federal Reserve beige book.

.jpg?crop=1.777xh:h;*,*&downsize=510px:*510w)

{kind=link}

Comments